FFO – Funds From Operations

A metric used to calculate operating performance

Updated:

July 3, 2023The difference between the intake of funds in the form of expenses and the funds from operations can be characterized as funds from operations.

Revenue from operations is the most common source of funds used to repay debts, buy assets, and pay dividends, taxes, and other expenses.

It is not intended to be a measure of cash flow because it eliminates working capital, capital expenditures, and other cash-flow adjustments, which are commonly misconstrued.

The amount of cash flow created by a company's business operations is known as FFO.

Depreciation, amortization, and losses on asset sales are added to earnings, then any gains on asset sales and interest income are subtracted. It is sometimes expressed as a per-share price.

To calculate net FFO

- Multiply net income by non-cash expenses or losses that are not incurred through operations, such as depreciation, amortization, and any losses on asset sales.

- After that, remove any capital gains and interest income.

A contentious topic is that a profitable business may not have sufficient finances after a year or term. Furthermore, businesses may have sufficient funds on hand yet still suffer a significant loss at the end of the year or period.

The profit and loss account records all expenses paid and outstanding and all income, which creates a paradox (received and accrued).

Furthermore, depreciation and amortization of intangible and fictional assets are not charged in the present period. They represent the distribution of historical expenses.

This means that while calculating net profit, the profit and loss account does not discriminate between fund flow and non-fund flow components.

The statistic real estate investment trusts (REITs) use to define the cash flow from their operations is called FFO. It is a metric used by real estate companies to assess their performance.

Companies that engage in Real Estate Investment Trusts (REITs), a business that focuses on income-generating real estate transactions, frequently employ it.

When examining REITs and other comparable investment trusts, the FFO-per-share ratio should be utilized instead of earnings per share (EPS).

Commercial real estate is sold, leased, and financed by REITs, which include office and apartment buildings, warehouses, hospitals, shopping centers, hotels, and timberlands.

- Funds from operations (FFO) reflect the difference between expenses and operational funds intake.

- Revenue from operations is commonly used to repay debts, buy assets, and cover expenses.

- FFO measures cash flow generated by business operations, excluding working capital and capital expenditures.

- FFO is used by real estate companies, particularly REITs, to assess their performance.

- FFO is not a substitute for cash flow but provides insights into a company's operational efficiency and profitability.

What Is Funds From Operations (FFO)?

FFOs are comparable to – but not identical to – cash from operations in that it is a reconciliation that starts with net income and adds back items in the same way as the indirect cash flow technique.

However, because it excludes working capital, capital expenditures, and other cash-flow adjustments, it is not intended to be a measure of cash flow.

1. EBITDA vs. FFO

It's similar to EBITDA in that it ignores working capital, but it's not quite the same. The main difference is that EBITDA tries to capture profitability from operations, whereas FFO is leveraged and captures the effect of taxes and preferred dividends.

2. Net operating income vs. FFO (NOI)

While net operating income (NOI) is a helpful profit indicator for assessing real estate down to the property level, it excludes general and administrative expenses, taxes, and leverage (interest expense), all of which are items that FFO considers.

Everything You Need To Build Your RE Modeling Skills

To Help You Thrive in the Most Rigorous RE Interviews and Jobs.

Formula and Calculation of Funds From Operations (FFO)

Unlike many non-GAAP metrics, FFO has an almost " official formula."

The formula for calculating funds from operations is shown below.

(Net Income + Depreciation + Amortization + Property Sales Losses) = FFO - Gains on Property Sales - Interest Income

The steps to calculate it are as follows:

The computation of all components on a REIT's income statement is listed.

Obtain the net income figure, which is the company's profit, at the bottom of the income statement.

The expensed components of a company's tangible (physical) and intangible assets for the period are depreciation and amortization.

Depreciation and amortization are accounting terms that assist organizations in spreading the cost of their assets out over time.

Net income for the accounting period is reduced by expenses. As a result, depreciation and amortization are added back to net income to calculate the REIT's actual incoming cash or revenue.

Add any losses on business property sales, if any. This usually refers to long-term assets like real estate, plants, and equipment.

These losses are deemed one-time and non-recurring and should not be included in the FFO calculation because they are not part of routine operations.

To calculate it for the period, subtract any gains or revenue gained from the sale of property from the total net income, depreciation, and amortization figure.

Subtract any interest earned by the company. Interest income is typically not a common element of a company's routine activities, so it should be excluded from the calculation.

Different Forms to calculate Funds From Operations (FFO)

You can use any of the following forms to calculate funds from operations:

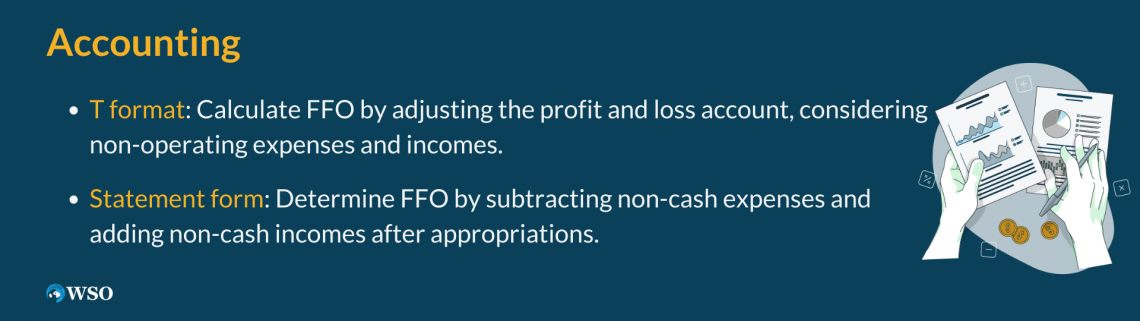

1. Account for profit and loss adjustments (T format)

The funds can be estimated in either account or statement format. An adjusted profit and loss account is prepared if given in the form of an account.

The account begins on the credit side with the opening profit balance and finishes on the debit side with the closing profit balance. If there is a loss, the debit side shows the opening balance, and the credit side shows the closing balance.

On the debit side are all non-operating expenses, and on the credit side are all non-operating incomes. The difference between the debit and credit sides is referred to as funds from operations.

The discrepancy between the credit and debit sides is known as funds lost in operation.

The following is the format for the adjusted profit and loss account:

| Particulars | $ | Particulars | $ |

|---|---|---|---|

| To balance b/d ( opening balance of loss) | By balance b/d ( opening balance of profit ) | ||

| To depreciation ( or depletion ) on fixed assets | By profit on sale of fixed assets | ||

| To goodwill written off | By profit on sale of long-term investments | ||

| To preliminary expenses written off | By dividend received | ||

| To discount on shares and debentures written off | By transfer from excess provision | ||

| To transfer to general reserve | By refund of tax | ||

| To patents, trade mark written off | By funds from operations ( balancing figure) | ||

| To dividend | By balance c/d ( closing figure of loss) | XXXX | |

| To premium on redemption of shares | |||

| To loss on sale of fixed assets | |||

| To provision for taxation | |||

| To funds lost in operations ( balancing figure) | |||

| To balance c/d ( closing figure of profit ) | XXXX | ||

| Total | XXXX | Total | XXXX |

Note that the statement will include either FFO or monies lost in operations. This is true for profit and loss account initial and closing balances as well (profit or loss).

2. Statement form

If the profit and loss adjustment account is prepared as a statement, the statement will begin with the profit and loss account's closing balance.

All expenses that do not result in a cash outflow are added to the profit, while all incomes that do not result in a cash inflow are removed.

After making all appropriations, if the profit is reported in the profit and loss account, the balance in the account at the beginning of the year must also be subtracted to arrive at money from the operation.

Below is a pro format:

| Particulars | $ | $ |

|---|---|---|

| Closing balance profit and loss account or retained earnings | xxx | |

| ADD: Item debited to P/L account for not resulting in an outflow of funds - | ||

| Depreciation on fixed assets | xxx | |

| Goodwill written off | xxx | |

| Preliminary expenses written off | xxx | |

| Discount on issue of shares written off | xxx | |

| Premium on redemption of shares | xxx | |

| Patents, trademarks written off, etc. | xxx | |

| Transfer to general reserve | xxx | |

| Transfer to any other specific reserve | xxx | |

| Loss on sale of fixed assets | xxx | |

| Loss on sale of long-term investments | xxx | |

| Provision for taxation (if it is not taken in current liabilities ) | xxx | |

| Interim/proposed dividend ( if it is appropriation and not taken as current liabilities) | xxx | xxx |

| LESS: Items credited to the P/L account not resulting in inflow ( regular or non-operating ) of funds- | xxx | |

| Profit on sale of fixed assets | xxx | |

| Profit on sale of long-term investments | xxx | |

| Dividend received | xxx | |

| Excess provision transferred back to P/L account | xxx | |

Refund of income tax | xxx

| xxx xxx |

| LESS: opening balance of profit and loss account ( credit) | xxx | |

| Funds from operations | xxx |

There is no set format; the format you choose is simply a question of personal preference.

What Funds From Operations (FFO) can tell you

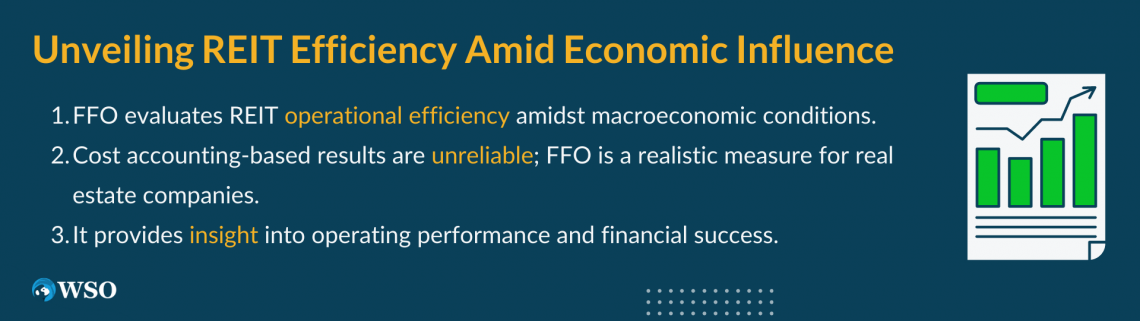

It evaluates a company's operational efficiency or performance, which is very important for REITs. This is because real estate values have been shown to rise and fall in response to macroeconomic situations

Operating results calculated using the cost accounting method are rarely accurate performance indicators.

It is a more realistic operating performance measure used by real estate enterprises. In addition, investors often use this statistic to assess a real estate company's financial success.

It measures a REIT's cash flow; real estate companies use it as a benchmark for operating performance. This non-GAAP measure was first introduced by the National Association of Real Estate Investment Trusts (NAREIT).

The cash flow from operations of a REIT, which is disclosed on the statement of cash flows, is not to be confused with the cash flow statement (CFS).

Instead, It calculates the net amount of cash and equivalents that a company receives from its regular, continuous operations. Therefore, it should not be used as a cash flow substitute or liquidity indicator.

For example, the money earned through an asset sale would affect a typical company's cash flow, but FFO does not include those profits. A specific company's CFS would also indicate a cash inflow if it got loan proceeds from a bank.

On the other hand, it excludes such cash inflows and is just a measure of revenue from business operations.

Why is FFO a good indicator of REIT performance?

It corrects for cost accounting practices that may misrepresent a REIT's genuine profitability. All REITs must depreciate their investment properties over time using one of the conventional depreciation methods, according to GAAP accounting.

Depreciation, on the other hand, is misleading in defining the worth of a REIT because many investment properties gain in value over time. Therefore, depreciation and amortization must be added back to net income to solve this problem.

Because these types of sales are deemed non-recurring, it subtracts any gains on property sales. Therefore, dividends and cash distributions to investors must account for 90% of all taxable income for REITs.

Gains on property sales do not contribute to a REIT's taxable income and should thus be excluded from valuation and performance calculations.

As previously stated, companies may give it per share as a supplement to their EPS.

These metrics also assist investors in determining if money is being spent wisely by management. The price-FFO ratio is also used by many analysts and investors as a supplement to the price-earnings ratio, which is the stock price divided by EPS.

The market price of a REIT would be divided by its FFO per share in the event of a REIT.

Net Income / Number of Outstanding Equity Shares = Earning Per Share

Why is FFO critical for REITs?

According to xxx, "Management considers it [which ignores accounting depreciation and gains/losses] an appropriate supplemental performance indicator" since "real estate values have traditionally risen or dropped with market circumstances."

REITs, in particular, are heavily leveraged and earn substantial non-cash income/losses from property sales. In their 10-K, BRE Properties explains why they use it:

Because REITs have distinct characteristics that make it difficult to analyze if investors rely simply on the other aforementioned standard measures of profits, it is a preferred metric for EBITDA, net income, or cash from operations.

Although FFO is not a widely accepted accounting principle, it might give investors a better understanding of a REIT's future returns than simply looking at net income or earnings per share. Depreciation is one of the fundamental reasons.

Depreciation is a financial concept that recognizes that any tangible object you purchase will lose value and effectiveness over time. While your older assets continue to age, newer assets enter the market.

As a result, even as the value of a piece of real estate rises over time, the improvements added to it (building, parking lot, fixtures) depreciate. Property owners can take an annual depreciation write-off as a result of this.

REITs, in particular, can deduct annual depreciation losses from their net income. Because of depreciation, capital gains and losses realized by the fund when selling assets (property) aren't a good forecast of how much income a REIT portfolio would earn.

Adjusted funds from operations

Analysts and REITs have begun to use somewhat modified forms of FFO, known as "adjusted FFO" or AFFO, over time. The rationale is that it includes nonrecurring items while excluding significant outflows such as capital expenditures.

Real estate experts are increasingly computing a REIT's AFFO. This computation takes a REIT's FFO and subtracts any capitalized and amortized recurrent expenses and any rent straight-lining.

Maintenance costs like painting or roof replacements are examples of ongoing capital expenditures. As a result, AFFO is becoming more popular as a more accurate predictor of a REIT's profit potential.

The AFFO metric was created to provide a more accurate picture of a REIT's cash flow or dividend-paying ability. This alternative measure is also known as money available for distribution or cash available for distribution (CAD) in addition to AFFO.

While there is considerable variation in how these are computed, the most common method is as follows:

FFO + nonrecurring expenses – capital expenditures = adjusted funds from operations

Example of How to Use FFO

On its 2017 income statement, popular mall REIT Simon Property Group reported $4 billion in funds from operations, up 6% from 2016. Meanwhile, the company's net income was $2.2 billion.

To arrive at it, the company deducted $1.8 billion in depreciation and amortization and adjusted for other smaller figures, such as a $5.3 million reduction for preferred distributions and dividends and a $17.1 million reduction for the noncontrolling interests portion of depreciation and amortization.

Simon also disclosed a $11.21 diluted FFO-per-share figure, compared to a $6.24 diluted EPS figure.

For instance:

- Last year, Big Time Real Estate Company reported a net income of $10 million, a $2 million depreciation expenditure, a $1 million interest amortization expense, a $500,000 interest income, and a $1 million profit on the sale of various properties.

- Big Time Real Estate Company's actual cash flow from business operations is $11.5 million.

- Calculate FFO for 2020 using account and statement format from the following balances derived from Goods Going Ltd.'s records.

| Particulars | 31st march 2019 ($) | 31st march 2020 ($) |

|---|---|---|

| Profit and Loss account | 600,000 | 900,000 |

| Provision for Dividends | 200,000 | 320,000 |

| General Reserve | 160,000 | 236,000 |

| Goodwill | 700,000 | 600,000 |

| Preliminary Expenses | 34,000 | 28,000 |

| Interest on Investments Received | 60,000 |

Solution

1. Account Format

| Particulars | $ | Particulars | $ |

|---|---|---|---|

| To Provision for Dividend | 120,000 | By balance b/d | 600,000 |

| To Transfer to General Reserve | 76,000 | By Interest Received on Investments | 60,000 |

| To Goodwill written off | 100,000 | By Funds from operations ( balancing figure ) | 542,000 |

| To Preliminary Expenses written off | 6,000 | ||

| To balance c/d | 900,000 | ||

| Total | 1,202,000 | Total | 1,202,000 |

2. Statement format

| Particulars | $ | $ |

|---|---|---|

| Closing balance ( Cr.) of Profit and Loss Account | 900,000 | |

| ADD: Non-operating charges already debited to P/L Account not resulting in outflow of funds | ||

| Goodwill written off | 100,000 | |

| Preliminary Expenses written off | 6,000 | |

| Transfer to General Reserve | 76,000 | |

| Transfer to Provision for Dividends | 120,000 | 302,000 |

| 1,202,000 | ||

| LESS: Non-operating Incomes already credited to P/L Account | ||

| Interest on Investments | 60,000 | |

| 1,142,000 | ||

| LESS: Opening balance of Profit and Loss Account | 600,000 | |

| Funds from operations | 542,000 |

Limitations of Funds From Operations (FFO)

The following are the operational fund limitations:

It excludes non-cash expenses like depreciation, asset depletion, and amortization.

If the business works on credit, it will be calculated inaccurately due to the products sold receipts credit approach utilized by many businesses.

Another factor for inaccurate calculations could be credit sales by the company during a recession.

Liquidity ratios are also more relevant than money from operations because they assess a company's ability to generate sufficient cash to repay debts in both good and bad times.

It excludes capital expenditures, which are a critical component of business expansion.

A cash flow statement cannot show a continual change in financial activities, such as working capital movements.

It is not an original statement because it is based on financial statements (i.e., the income statement and balance sheet).

Because it is a historical statement, predicted funds flow statement may not necessarily give highly accurate forecasts of the financial condition.

It does not replace financial statements, such as the Income Statement and Balance Sheet. It merely provides information on the change in working capital position, which is dependent on the financial statement data.

The Cash Flow Statement, which shows changes in cash position, is more important or instructive than the one that shows changes in working capital.

Funds From Operations (FFO) FAQ

The difference between the intake of funds in the form of expenses and the FFOs can be characterized as FFO. Revenue from operations is the most common source of funds used to repay debts, buy assets, and pay dividends, taxes, and other expenses

Adjusting the profit and loss account for non-fund flow items yields FFO. Before removing cash spent on day-to-day business, the adjusted profit and loss will represent income from operational activities.

In other words, it simply indicates cash inflow from the company's usual operations, such as inventory, trade receivables, and other assets.

Adjusted earnings are used in EPS to guarantee that they are equivalent to FFOs. Both phrases are similar since knowing an organization's ability to create cash is critical.

While it is commonly employed for examining REITs, traditional property-level real estate profit indicators are also very relevant, namely:

- It gives a levered measure of profit after taxes and expenses, whereas,

- NOI provides a pure, property-level measure of profit.

- Cap rates are the most generally used measure of value in real estate for REIT valuation and property-level research. It's the same as valuing "normal" corporations with EV/EBITDA multiples.

Everything You Need To Break into Venture Capital

Sign Up to The Insider's Guide by Elite Venture Capitalists with Proven Track Records.

Researched and authored by Deeksha Pachauri | LinkedIn

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?